GUEST POST by Todd N. Tucker, Research Fellow at the Roosevelt Institute.

GUEST POST by Todd N. Tucker, Research Fellow at the Roosevelt Institute.

A major thrust of President Obama’s pitch for the Trans-Pacific Partnership agreement, or TPP, is geopolitical. As the president himself put it last year,

The world has changed. The rules are changing with it. The United States, not countries like China, should write them. Let’s seize this opportunity, pass the Trans-Pacific Partnership and make sure America isn’t holding the bag, but holding the pen.

In other words: there’s a race for influence in the Asia-Pacific between the U.S. and China. Only one can win. Either China sets the rules, or the U.S. does. If China gets there first, their rules will prevail.

This story seems to assume that the rules the countries would set are different. Is this true?

We don’t have to guess. Wolfgang Alschner and Dmitriy Skougarevskiy are the brains behind the website Mapping Investment Treaties. The site allows text-as-data comparisons between thousands of ratified and proposed international treaties. In an article published earlier this year, Wolfgang and Dmitriy concluded:

China is likely to be most sympathetic to a multilateralization of investment disciplines around TPP. The country is among the states that have concluded most investment agreements. Moreover, its recent BIT with Canada overlaps textually to 50% with the TPP and converges in substance in some areas. When it comes to MFN, for instance, the China–Canada BIT is the closest treaty to TPP in our database.

That said, they go on to note several differences between the U.S. and Chinese templates.

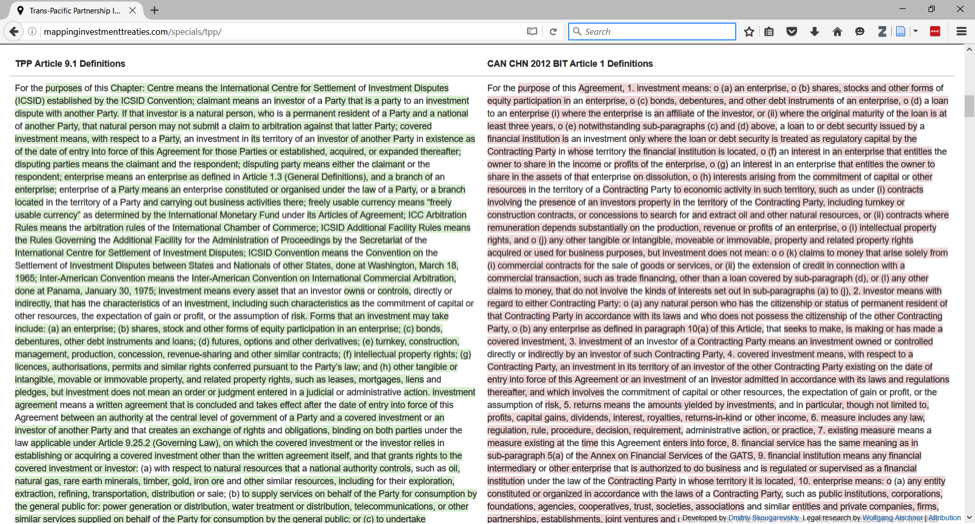

I wanted to know just how different the two pacts where, so I asked this legal power duo to create a special feature on their website to allow the rest of us to compare Obama’s TPP with the Canada-China bilateral investment treaty, or BIT, which was signed in 2012 and entered into force in 2014. Thankfully, they agreed. To see the side-by-side, go to this website. Where it says “From Abstract Metric to Textual Comparison,” hover over the dropdown menu just before the treaty text and scroll down to “Treaties of Special Interest,” and then “Canada-China BIT (2012).”

The side-by-side is really helpful, and highlights some of the limitations of any text-as-data methodology. As is evident from the screenshot below, a lot of text passages are considered divergent when in fact they are merely in a different order or use slightly different country-specific verbiage. This type of variation is what leads Wolfgang and Dmitriy to conclude that the two pacts are only 50 percent alike. If a team of human lawyers were to go visually through the provisions, this percentage would be substantially higher. That’s not a criticism of their approach, just an argument for supplementing it with manual analysis.

What can we conclude?

What can we conclude?

Rules are often similar…

Scrolling down, it becomes clearer that most of the controversial provisions are effectively the same. For instance, both pacts require “fair and equitable treatment,” a capacious standard that has been interpreted as including a freezing of the regulatory environment. Both require national courts to defer to the decisions of ad-hoc investment tribunals set up outside of national legal systems.

Finally, a protected investment is defined in both as involving “the commitment of capital or other resources, the expectation of gain or profit, or the assumption of risk.” This, coupled with language on compensating investors for the “fair market value” of their investments, is part of what allows investors to claim damages for lost profits. While national legal systems allow this remedy in tort claims between private parties, it’s rarer in claims against government under domestic law. These provisions are hotly sought by U.S.-incorporated companies, but it is unclear if and how they benefit U.S. workers.

…Except where Chinese rules are less investor-friendly…

There are some provisions where the China pact is more protective of the public interest than the TPP promoted by Obama.

Take the rules on national treatment. In the China pact, foreign investors are only required to be treated as well as nationals once they are in the market. The TPP, by comparison, requires what is known as “pre-establishment” national treatment. This means that regulators have to allow the “establishment [and] acquisition” of investments in the first place. Some critical observers have argued this impinges on the development planning and screening capacity of states.

Similarly, the rules on “fair and equitable treatment” in the China BIT do “not require treatment in addition to or beyond that which is required by the international law minimum standard of treatment of aliens as evidenced by general State practice accepted as law” (emphasis added). Translated into plainer English, the China treaty obligates arbitrators to look to what states do in the real world to establish norms, as opposed to what ad hoc arbitrators say they do. (For a primer on these issues, see Matt Porterfield’s piece here.)

Finally, the rules on performance requirements are much more pro-regulation in the China-Canada BIT. While the TPP’s Article 9.10 places limits on how much states can Buy Local, the China-Canada BIT adopts the relatively looser rules of the World Trade Organization.

As Timothy Lee at Vox joked on Twitter last year, if the TPP is about U.S. or Chinese rules winning, maybe we would be better off ceding the contest.

…But it won’t matter anyway.

Up until now, I’ve assumed that it actually matters which set of rules is better. However, the better or worse provisions may not lead to different standards of treatment. Both pacts have most-favored nation rules that allow investors to claim the most investor-friendly treaty provisions. Both allow investors to claim to be from a “home country” simply through changing their corporate registration. Indeed, thanks to the China-Canada agreement, Chinese and U.S. investors already have ample rights in each other’s markets. All they need to do is channel their cross-Pacific investments through Canadian holding companies. This state of affairs already holds, with or without the TPP.

This is why I and others have deemed growth-by-bilateral/regional-agreements a form of creeping multilateralization. With this setup, it’s not China or the U.S. setting the rules in the Asia-Pacific: it’s investors claiming the rules they like the most in the whole treaty network.

Of course, TPP proponents’ geopolitical sales pitch could refer to rules besides investment. For instance, I anticipate TPP proponents will tout the treaty’s expansive rules on labor standards. In contrast, China’s agreements are generally seen as being less prescriptive on this front.

It’s unclear to me whether this distinction will matter on the ground. The TPP’s labor rules unquestionably have weaker enforcement provisions than the investment rules, and have not attracted unconditional support from labor rights groups.

In any case, for the time being, we don’t have good text-as-data comparisons for non-investment provisions. Scholars like Alschner, Todd Allee, Zach Korman, and others are leading efforts to make comparisons more accessible across a broader range of TPP chapters. This will allow for greater public scrutiny of the distance between Chinese and U.S. templates.

So what’s this all about?

There’s a different type of geopolitical justification for the TPP, one that is more agnostic toward the actual content of the treaties. For instance, W.K. Winecoff and colleagues have argued that there is a race between countries to see who can be at the center of treaty networks. Connected to this is the credibility-based notion that democracies with separation of powers need to show their less democratic rivals that they are equally capable of following through on their commitments. Ergo, if Obama signs the TPP but can’t deliver congressional ratification, the U.S. looks weak.

But this isn’t so much an argument for the TPP as it is for any form of international cooperation. The U.S. could sign climate, tax avoidance, or even cultural exchange agreements: All would add to treaty density. If this is the strategy, it would be smarter to discard highly complex and controversial agreements like the TPP, and instead simply sign as many low-hanging-fruit agreements as possible, so Team U.S.A. would look as capable as possible.

There is a more fundamental reason to be skeptical about the TPP impacting Chinese-U.S. competition in the Asia-Pacific. Even if the TPP were to include meaningful international law commitments, they would be just that: international (weakly enforceable) law, not national (highly enforceable) law. Both China and the U.S. have highly malleable attitudes towards international law. The U.S. has followed international legal orders mostly when they were already consonant with national security strategy. And China has recently flouted the rulings of an international arbitration panel on its maritime dispute with the Philippines. Far from affecting China’s behavior, the ruling seems to have emboldened belligerents within China. We shouldn’t expect from international law more than it can deliver.

In closing, there is a risk to the saber-rattling rationale for an agreement that will change so little of the economic or national security fundamentals. As Joseph Stiglitz has argued,

Such rhetoric, reminiscent of Cold War containment strategies, is not constructive for the world’s most important bilateral relationship. The truth is that this strategic rationale for TPP makes little sense.

With China now the world’s largest economy in terms of output (measured in purchasing power parity), trade, and source of foreign direct investment, the ship has sailed on containing China’s influence. This should have been obvious from last year’s failed attempt by U.S. policymakers to block the Asian Infrastructure Investment Bank, created under China’s leadership.

If trade deals were all that mattered for securing influence, the United States could at best hope for a stalemate with China, which already has agreements with more than half of TPP partners, among other nations. What matters for influence is not just signing agreements but the depth and nature of relationships. Given the hundreds of billions of dollars China has committed to finance infrastructure development across the region and the magnitude of China’s trade and investment integration with the world, there is little reason to think that implementation of TPP would tip the balance of economic power in the U.S.’s favor.

Todd N. Tucker is a Roosevelt Fellow. His interests revolve around global economic governance, including dispute settlement and the domestic regulatory implications of international trade, investment, and tax treaties. The original version of the post appeared here.

While all attention is focused on mega-regional negotiations, European states are quietly beginning to redesign their national investment treaty programs. The recent

While all attention is focused on mega-regional negotiations, European states are quietly beginning to redesign their national investment treaty programs. The recent  Textual similarity analysis offers a new way to investigate who wins treaty negotiations. But not every deviation from a prior agreement or a country’s model treaty is a concession.

Textual similarity analysis offers a new way to investigate who wins treaty negotiations. But not every deviation from a prior agreement or a country’s model treaty is a concession.